On May 29, at the 2025 SMM (2nd) Rare Earth Industry Forum hosted by SMM Information & Technology Co., Ltd., Gao Yazhou, Director of the Motor Technology Department at the R&D Center of Goldwind Science&Technology Co., Ltd., shared the topic of "Rare Earths & Wind Power: Empowering Carbon Neutrality" with the attendees.

Development Trends in the Wind Power Industry

[Wind Power Industry Trends] The Global Wind Power Industry Looks to China, Stepping Boldly into the Carbon Neutrality Era

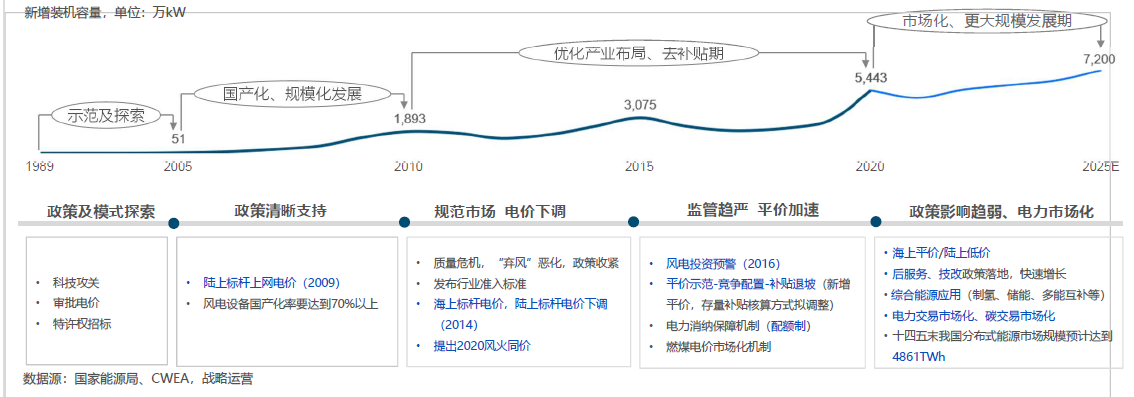

• With clear "dual carbon" goals, the wind power market is entering a period of historic opportunities. The cumulative new installations during the "14th Five-Year Plan" period will reach 250-300 million kW, an 80% increase compared to the "13th Five-Year Plan" period, with an average annual installation of 50-60 GW.

• By 2030, installations will reach at least 800 million kW, and by 2060, at least 3 billion kW, indicating that wind power will maintain rapid and sustained development over the next 40 years!

[Wind Power Industry Trends] In China, Wind and Solar Installations Surpass Thermal Power

In Q1 2025, China's combined new installations of wind and PV power reached 74.33 million kW, with cumulative installations reaching 1.482 billion kW (including 536 million kW of wind power and 946 million kW of PV power), surpassing thermal power installations (1.451 billion kW) for the first time. In the future, as new installations of wind and PV power continue to grow rapidly, it will become the norm for wind and PV installations to exceed thermal power installations.

In Q1, the combined power generation from wind and PV reached 536.4 billion kWh, accounting for 22.5% of the total electricity consumption in society, with non-fossil energy power generation accounting for 39.8%.

In Q1, the combined power generation from wind and PV increased by 111 billion kWh compared to the same period last year, significantly exceeding the increase in total electricity consumption in society (58.2 billion kWh).

[Wind Power Industry Trends] Wind Power is Playing a Pivotal Role in the Social Economy

Annual output value is approximately 600 billion yuan, with an employment base of about 2.5 million people.

Complete industry chain: covering wind resource assessment, wind farm development and construction, equipment manufacturing, technical services, testing and certification, investment and financing services, etc.

Feeding back into related industries: driving progress and breakthroughs in materials technology, testing and inspection, heavy-haul transportation, and other sectors.

[Wind Power Industry Trends] China has Become the World's Largest Wind Power Equipment Manufacturing Base

China accounts for 50% of the global market share in the production of wind turbine parts and complete machines; key components and castings and forgings account for 70% of global market production (e.g., generators, wheel hubs, frames, blades, gearboxes, bearings, etc.).

[Wind Power Industry Trends] Innovation in Materials, Technology, Standards, and Models is Becoming Normalized

With the further reduction in the price of wind turbines, the industry is building a new technological system through technological advancements in new theories, materials, processes, core components, and architectures across the four areas of "wind"-"turbine"-"farm"-"grid".

"Trends in the Wind Power Industry" Major Trends in Wind Turbines: Larger Rotors, Higher Capacity

• Major Trend - Larger Rotors and Higher Capacity: As the scope of wind energy resource development and utilization in China continues to expand, the development of low-wind-speed resources in southeastern China has become a significant trend. The technological development of wind turbines is also gradually aligning with this demand, showing a trend towards larger rotors and higher capacity.

• In 2024, the world's longest GW147-meter blade passed static testing in one go. From 2022 to 2024, the unit capacity of wind turbines has increased from 16 MW to 26 MW, with Goldwind's 16 MW turbines already achieving mass offshore operation.

"Trends in the Wind Power Industry" Major Trends in Wind Turbines: Taller Towers

• Major Trend - Larger Rotors and Taller Towers: As the scope of wind energy resource development and utilization in China continues to expand, the development of low-wind-speed resources in southeastern China has become a significant trend. The technological development of wind turbines is also gradually aligning with this demand, showing a trend towards larger rotors and taller towers. In terms of tower height, since Goldwind began experimenting with steel-concrete hybrid tower structures in 2013, the technology for tall flexible steel towers and hybrid towers has continuously pushed the height of tower bases, with the benchmark height of domestic towers increasing from 120 meters (steel-flexible tower) in 2015 to 185 meters (steel-concrete hybrid tower) in 2024.

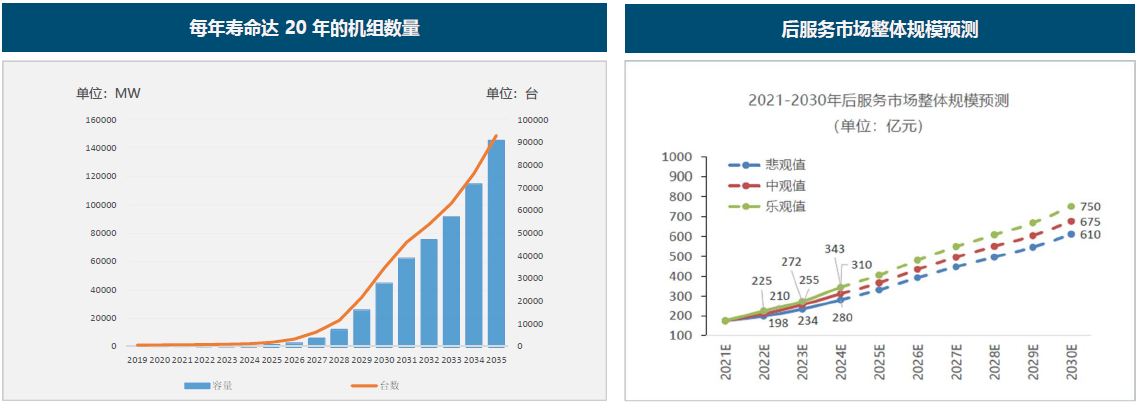

"Trends in the Wind Power Industry" Broad Prospects for the Retrofitting and Replacement Market

• Market Size Forecast for After-Sales Services: The after-sales service market for wind power is expected to enter a golden period of rapid growth in out-of-warranty capacity over the next three years. With the accelerated pace of wind power technology upgrades, there is a significant demand for retrofitting and replacing aging turbines, indicating broad prospects. It is estimated that by 2024, the cumulative out-of-warranty capacity will reach 229 GW, with the overall market size of after-sales services being approximately 31 billion yuan. Calculating at a 25% openness rate for operation and maintenance in 2024, the effectively open market size will be approximately 20 billion yuan.

• Policy Support: The National Energy Administration has released a draft for public comment on the "Administrative Measures for the Retrofitting, Upgrading, and Decommissioning of Wind Farms," officially providing clear and traceable policy support for the technological retrofitting and upgrading of aging wind turbines. It encourages the systematic upgrading and optimization of wind farms with unit capacities less than 1.5 megawatts (MW) or that have been in operation for more than 15 years.

Challenges and Demands

"Challenges and Demands" Continuous Decline in Wind Turbine Bid Prices and Soaring Prices of Rare Earths

• Market Price Trends of Wind Turbines: Since 2021, China's onshore wind power market has gradually entered a phase of low-price competition. As of November 2024, the lowest market price for onshore wind turbines (including towers) was 1,355 yuan/kW (data source: Fengmang Energy).

• Price Trends of Pr-Nd Metal Oxides: The nearly threefold price surge from 2021 to 2022 has imposed significant cost pressure on direct-drive permanent magnet wind power technology, promoting a rapid transition towards medium-speed permanent magnet wind power and high-speed doubly-fed induction generator (DFIG) wind power technology routes. Although there was a pullback in 2024, due to the medium-speed industry chain and the cycle of delivery rhythm, it is difficult for the direct-drive technology route to reverse course in the short term.

"Challenges and Requirements" - Suitable Scenarios for Different Wind Power Technology Routes

• Low-speed motors without gearboxes: Permanent Magnet Synchronous Generators (PMSGs) and Electrically Excited Generators (EEGs), with rated speeds ranging from 7.5rpm to 15rpm.

• PMSGs matched with low transmission ratio (40-80) gearboxes, with rated speeds ranging from 200rpm to 600rpm.

• Motors matched with high transmission ratio (100-150) gearboxes: Doubly-Fed Induction Generators (DFIGs), Squirrel Cage Induction Generators (SCIGs), and PMSGs, with rated speeds ranging from 1700rpm to 1800rpm.

• DFIG is currently the most economical technology route for onshore wind power; medium-speed PMSG is the most suitable technology route for offshore wind power at present; and direct-drive PMSG is the most reliable technology route (Siemens offshore units).

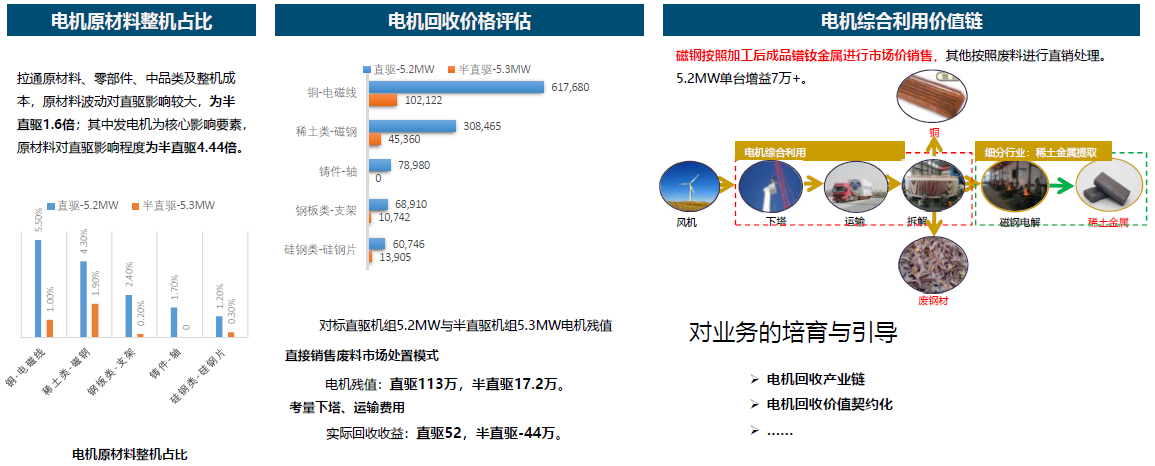

"Challenges and Requirements" - Business Model Innovation and Value Potential of Direct-Drive Motors

• Comparing the residual values of 5.2MW direct-drive and 5.3MW semi-direct-drive motors, and considering the direct sales and scrap market disposal models, as well as the costs of tower dismantling and transportation, the recoverable revenue for direct-drive motors is 520,000 yuan, while for semi-direct-drive motors, it is -440,000 yuan. Copper and rare earth materials account for the largest portion of the residual value, exceeding 80%.

• Rare earths are non-renewable elements with significant market value and application prospects. Disposing of them as processed Pr-Nd alloy products will yield an additional gain of over 70,000 yuan per unit.

• Innovative business models, such as a professional wind turbine motor recycling industry chain and contractualized motor recycling value, need to be cultivated and guided within the industry.

In addition, it provides a detailed discussion on Goldwind's permanent magnet motors.

》Click to view the special report on the 2025 SMM (2nd) Rare Earth Industry Forum